The fixed vs. variable debate is heating up again in 2025—and for good reason. Borrowers across Canada are asking: should I lock in a fixed rate for stability, or ride the wave with a variable rate that could drop even further? <br> The truth? There’s no universal answer—especially in a year where the economy could swing in either direction.

As of May 1, 2025, the Bank of Canada’spolicy rate sits at 2.75%, with a prime rate of 4.95%. Based on market expectations,both are likely to trend downward by year’s end.

Here’s what we could be looking at:

Meanwhile, 5-year fixed rates for insured mortgages (minimum down payment,owner-occupied homes) are forecasted to land between 3.82% and 4.00%.

So far, variable appearsto offer slightly lower rates—but that comes with one big catch: no guarantees.These forecasts shift as quickly as the economy does.

Note: All rates above are insured and for illustrativepurposes only. They’re subject to change without notice, and actual offers varyby lender.

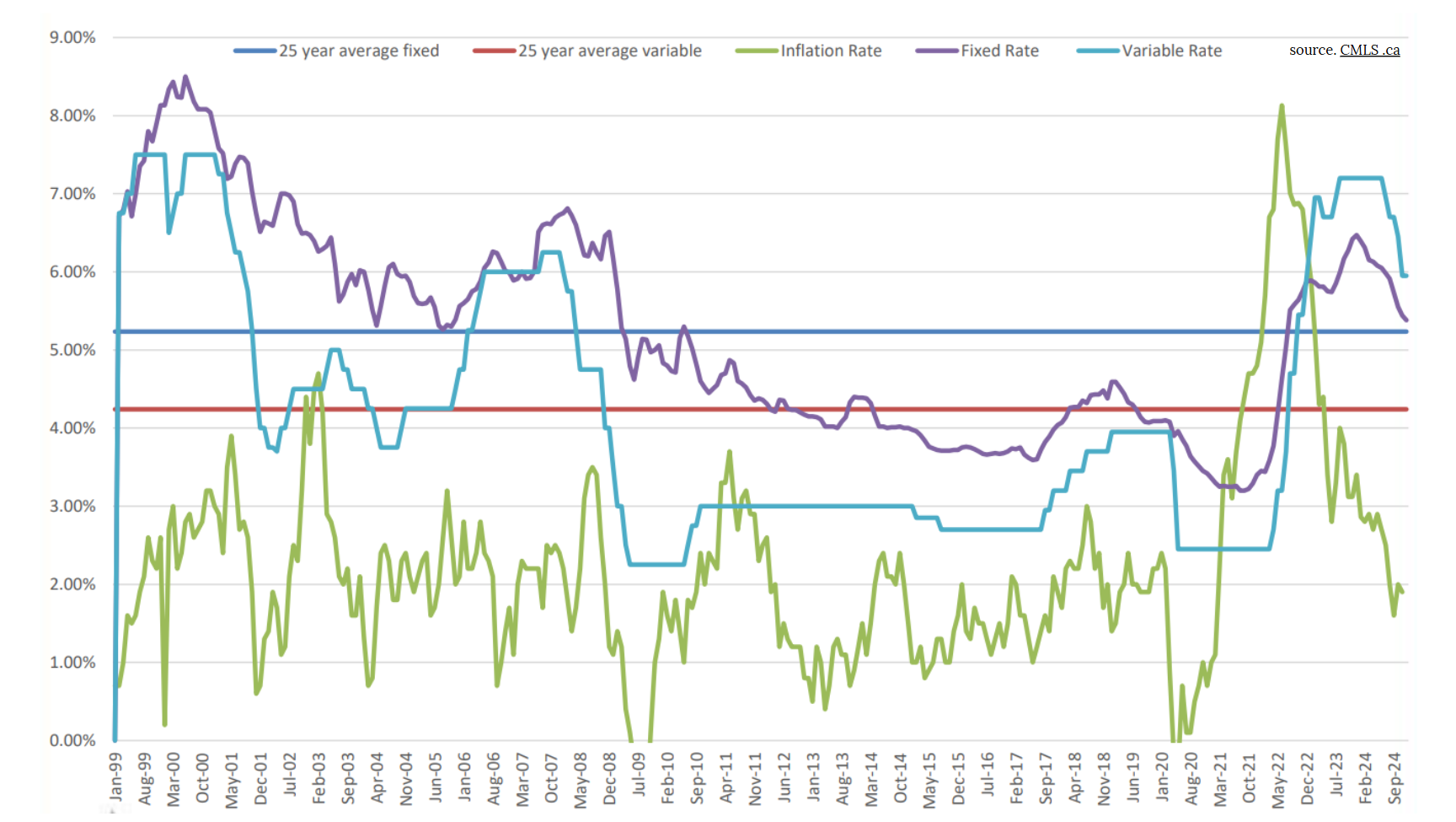

Back in 2020, when COVID hit, many expertspredicted a housing crash. Instead, we saw one of the most aggressive realestate booms in Canadian history. Rates dropped to record lows, demandexploded, and those who chose variable mortgages often came out ahead.

We could be heading into a similarsituation. If Canada experiences a mild recession (or even a full one),interest rates typically fall further. That could spark a return of buyeractivity—and possibly even another wave of housing competition.

But there's also a real chance we enter a moretraditional downturn, where both prices and demand cool off. Either way, timingthe market perfectly is next to impossible.

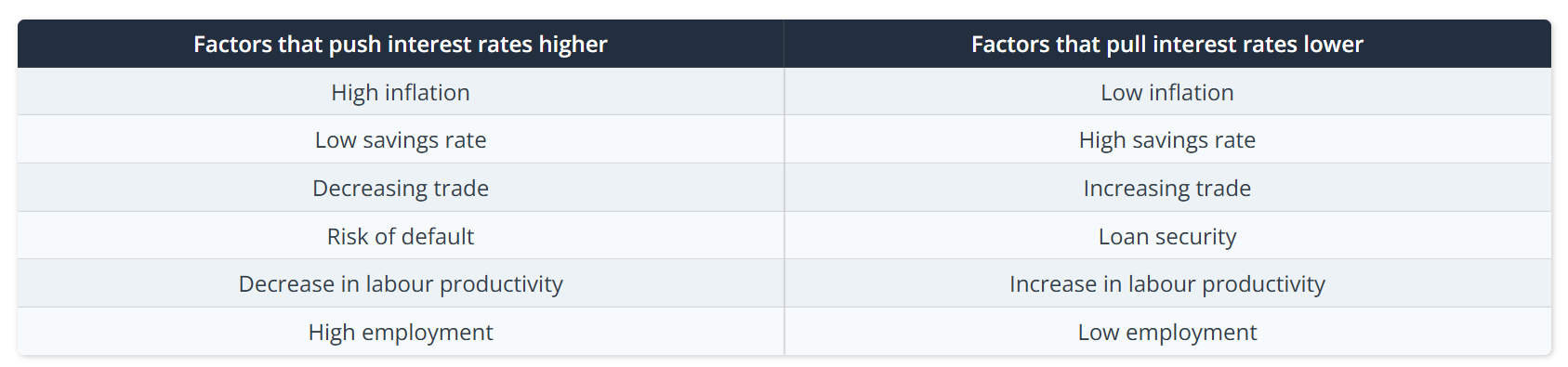

Here’s a side-by-side tohelp you decide what might be best for your situation:

Quick tip:Historically, variable rates have outperformed fixed more often than not—but only when borrowers stayed the fullterm and didn’t break the mortgage early.

Source: wowa.ca

These numbers reflectinsured rates, and assume a steady term and risk premium. Real-worldconditions—like inflation surprises, global instability, or policychanges—could shift these projections quickly. And honestly, the 5-year fixesseem a bit optimistic to me as well!

No one can say for sure where the marketis heading. Not economists, not central banks, not even the traders pricing infuture cuts. All we can say with certainty is that mortgage strategy should be based on your goals—not someone else’sforecast.

If you value peace of mind and budgetingcertainty, fixed may be the way to go. If you’re comfortable riding the ratewave and want the potential to save over time, variable could be worth the risk.

In a world of economic uncertainty, one thing remainsconstant: making the right choice starts with a conversation.

I’ll help you comparetoday’s best variable and fixed rates side by side, based on your income,timeline, and comfort with risk—so you can feel confident in whichever path youchoose.

📞 647-980-5399

📧 alex@ontariomortgageexpert.ca

Sources: